FAQ

Q: What is the Group Retirement Program?

The Group Retirement Program is a Syndicate program meant to help small businesses group together to have access to more affordable and robust 401(k) investment options.

Q: How do Syndicates work?

Syndicate pricing in 401(k) plans occurs when multiple employers come together to negotiate lower investment and administrative fees. By combining purchasing power, they access institutional share classes and reduced costs, helping improve participant outcomes while maintaining fiduciary oversight and plan flexibility.

Q: What are the Benefits of joining our Syndicate?

1. Negotiated group pricing - See home page for pricing

2. No start-up fee to the employer

3. No document fee to the employer

4. No annual 5500 filing fee to the employer

5. ERISA Bond Included

6. Investments are monitored and replaced if required; quarterly

7. Employees' education and tools given for financial literacy and saving success.

8. Custom plan design

9. Reduce employer fiduciary liability

10. Plan price comparison at no charge

11. Employer contributions and expenses are tax-deductible. See your tax professional.

12. No loan, distribution, or termination fee

Q: Why consider a Syndicate plan?

A Syndicate 401(k) plan allows employers to come together to reduce fees, access institutional investments, and strengthen fiduciary oversight. The result is lower costs, improved participant outcomes, and simplified plan management—without sacrificing flexibility or control.

Q: My business currently has a 401(k) or another retirement contribution plan. should my company consider utilizing the Group Retirement Program?

Yes, The Group Retirement Program is an efficient and affordable program that will give you more time back, help your employees prepare for retirement, and allows for the takeover of many of your fiduciary responsibilities.

Q: What are some features of the Group Retirement Program?

1. Auto-enroll: Those not already enrolled will be auto-enrolled into the plan. *

2. Auto escalation: Increases contribution by 1% each year up to 10%. *

3. 3(16) Fiduciary: transfers the administration liability to a third party.

4. 3(38) Fiduciary: investments are monitored and replaced with discretion.

5. Payroll integration (depending on payroll provider). *

6. Your company logo on enrollment flyer.

7. You may customize our education program and time allowance.

* Only available for those who have API or True 360 payroll integration

Q: Who can join?

All businesses who are members of the Vegas Chamber are welcome, including those out of state.

Q: How much can my company save in fees by servicing my 401(k) plan with the Group Retirement Program?

With our proposal, we provide a side by side comparison with what you currently have as a plan against what we provide through the Group Retirement Program.

Q: What is the timeline for a company to initiate a retirement plan (Generally)?

If all census information and required documents are provided, the ETA of implementation is within 30 to 60 days, given required notices.

Q: What are the investment options?

The program will offer both passive and active investment options, reviewed for performance, fees and other factors.

Q: Who selects the investment options?

Joe Caldera selects and monitors the investment line-up as the 3(38)-investment fiduciary.

Q: How are investment options chosen?

It is our fiduciary responsibility to select and offer top-tier investment options available. To choose these offering all investments are screened, selected, monitored and scored every three months on a 12- point system.

Q: Who holds the investments?

Matrix Trust Company, a subsidiary of Broadridge Financial Solutions

Q: What are Recordkeepers and what do they provide?

Recordkeepers track the activity, and the participants' balance in the plan, which includes deposits, withdrawals, loans, and investments. Often, the recordkeeper is also the custodian, who physically holds the retirement assets.

Q: What are Third Party Administrators and what do they provide?

Third Party Administrators create the company's governing documents, prepare required notices to employees, manage loans and distributions. They also complete the annual testing and IRS filings.

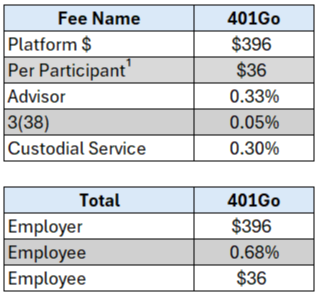

Q: What are the expenses?

1 - Fees Per Enrolled Employee can be participant Paid or Employer Paid

An independent audit is required for employers with 100 or more participants who have account balances. Each employer must engage their own auditor, including payment.

Q: What about distributions or loans?

The TPA will review and authorize any distribution requests from participants in your 401(k) plan. This will also include loan reviews and authorization if your plan includes loan provisions. There is no need to worry about pesky emails flooding your inbox asking for a signature.

Q: What are my responsibilities as a sponsor under the Group Retirement Program?

Your responsibilities include uploading pay files (unless payroll is integrated) and providing year-end data. Speak with an ERISA attorney and fiduciary insurance liability agent about your responsibilities and liability. Employers are responsible for selecting and monitoring their providers. The Vegas Chamber does not serve as the fiduciary on your plan.

Q: Which payroll providers are currently providing Integration?

401Go can work with most payroll providers.

- API: iSolved, Execupay, Paylocity, Gusto, Quickbooks Online, Rippling, Coastal, EddyHR, Auris, & Paycor.

- True 360 Team (401Go): ADP Run, Paychex, Paycom, Fingercheck, & BambooHR.

- Manual: Quickbooks Desktop

Payroll providers are subject to change. Please contact us directly to see if we can integrate with your payroll provider.

Q: Can I customize plan provisions?

Yes, you can select eligibility by age and length of service. You can also offer a safe-harbor match or discretionary match.

Q: What are the Safe Harbor and matching options?

1. 100% up to 3% of compensation to all those who are eligible

2. 100%, up to 6% match of compensation of those who defer

3. 100%, up to 3%, and 50% on the next 2% deferral based on compensation.

4. 100%, up to 1%, and 50% on the next 5% deferral based on compensation.

5. Discretionary match or no match (Non-Safe harbor)

Any match provided is based on total compensation, including employee bonuses. Must pass ADP & ACP testing.

Q: How do you get started, and who helps with enrollments?

Contact Joe Caldera LPL Financial Advisors, at (702) 846-4015 or (702) 846-401(k) or ARP@calderawealth.com.

Caldera Wealth and LPL Financial are not affiliated with any of the above named entities.